Code of numerical experiments in this paper.

@misc{gierjatowicz2020robust,

title={Robust pricing and hedging via neural SDEs},

author={Patryk Gierjatowicz and Marc Sabate-Vidales and David Šiška and Lukasz Szpruch and Žan Žurič},

year={2020},

eprint={2007.04154},

archivePrefix={arXiv},

primaryClass={q-fin.MF}

}

...

The file Call_prices_59.pt contains the target Vanilla call option prices generated with Heston model for bi-monthly maturities up to 1 year, and 21 different strikes between K=0.8 and K=1.2.

Heston model parameters:

Resulting target IV surface:

-

nsde_LV.py: Calibration to target prices of Neural SDE using Local Volatility model.python nsde_LV.py --device 0 --vNetWidth 50 --n_layers 20 -

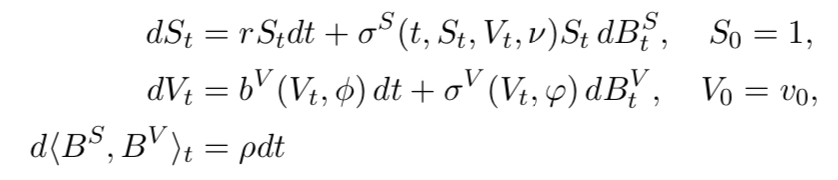

nsde_LSV.py: Calibration to target prices of Neural SDE using Local Stochastic Volatility model, where \sigma^S, b^V and \sigma^V are feed-forward neural networks:

python nsde_LV.py --device 0 --vNetWidth 50 --n_layers 20