EconML is a Python package for estimating heterogeneous treatment effects from observational data via machine learning. This package was designed and built as part of the ALICE project at Microsoft Research with the goal to combine state-of-the-art machine learning techniques with econometrics to bring automation to complex causal inference problems. The promise of EconML:

- Implement recent techniques in the literature at the intersection of econometrics and machine learning

- Maintain flexibility in modeling the effect heterogeneity (via techniques such as random forests, boosting, lasso and neural nets), while preserving the causal interpretation of the learned model and often offering valid confidence intervals

- Use a unified API

- Build on standard Python packages for Machine Learning and Data Analysis

In a nutshell, this

toolkit is designed to measure the causal effect of some treatment variable(s) T on an outcome

variable Y, controlling for a set of features X. For detailed information about the package,

consult the documentation at https://econml.azurewebsites.net/.

Table of Contents

One of the biggest promises of machine learning is to automate decision making in a multitude of domains. At the core of many data-driven personalized decision scenarios is the estimation of heterogeneous treatment effects: what is the causal effect of an intervention on an outcome of interest for a sample with a particular set of features?

Such questions arise frequently in customer segmentation (what is the effect of placing a customer in a tier over another tier), dynamic pricing (what is the effect of a pricing policy on demand) and medical studies (what is the effect of a treatment on a patient). In many such settings we have an abundance of observational data, where the treatment was chosen via some unknown policy, but the ability to run control A/B tests is limited.

|

Businesses offer personalized incentives to customers to increase sales and level of engagement. Any such personalized intervention corresponds to a monetary investment and the main question that business analytics are called to answer is: what is the return on investment? Analyzing the ROI is inherently a treatment effect question: what was the effect of any investment on a customer's spend? Understanding how ROI varies across customers can enable more targeted investment policies and increased ROI via better targeting. |

|

Personalized discounts have are widespread in the digital economy. To set the optimal personalized discount policy a business needs to understand what is the effect of a drop in price on the demand of a customer for a product as a function of customer characteristics. The estimation of such personalized demand elasticities can also be phrased in the language of heterogeneous treatment effects, where the treatment is the price on the demand as a function of observable features of the customer. |

|

Which patients should be selected for a clinical trial? If we want to demonstrate that a clinical treatment has an effect on at least some subset of a population then fully randomized clinical trials are inappropriate as they will solely estimate average effects. Using heterogeneous treatment effect techniques, we can use observational data to come up with estimates of these effects and identify good candidate patients for a clinical trial that our model estimates have high treatment effects. |

|

In the design of a page layout and ad placement, it is important to understand the click-through-rate of page components on different positions of a page. Modern approaches may be to run multiple A/B tests, but when such page component involve revenue considerations, then observational data can help guide correct A/B tests to run. Heterogeneous treatment effect estimation can provide estimates of the click-through-rate of page components from observational data. In this setting, the treatment is simply whether the component is placed on that page position and the response is whether the user clicked on it. |

September 4, 2020: Release v0.8.0b1, see release notes here

Previous releases

March 6, 2020: Release v0.7.0, see release notes here

February 18, 2020: Release v0.7.0b1, see release notes here

January 10, 2020: Release v0.6.1, see release notes here

December 6, 2019: Release v0.6, see release notes here

November 21, 2019: Release v0.5, see release notes here.

June 3, 2019: Release v0.4, see release notes here.

May 3, 2019: Release v0.3, see release notes here.

April 10, 2019: Release v0.2, see release notes here.

March 6, 2019: Release v0.1, welcome to have a try and provide feedback.

Install the latest release from PyPI:

pip install econml

To install from source, see For Developers section below.

Double Machine Learning (click to expand)

- Linear final stage

from econml.dml import LinearDMLCateEstimator

from sklearn.linear_model import LassoCV

from econml.inference import BootstrapInference

est = LinearDMLCateEstimator(model_y=LassoCV(), model_t=LassoCV())

### Estimate with OLS confidence intervals

est.fit(Y, T, X, W, inference='statsmodels') # W -> high-dimensional confounders, X -> features

treatment_effects = est.effect(X_test)

lb, ub = est.effect_interval(X_test, alpha=0.05) # OLS confidence intervals

### Estimate with bootstrap confidence intervals

est.fit(Y, T, X, W, inference='bootstrap') # with default bootstrap parameters

est.fit(Y, T, X, W, inference=BootstrapInference(n_bootstrap_samples=100)) # or customized

lb, ub = est.effect_interval(X_test, alpha=0.05) # Bootstrap confidence intervals- Sparse linear final stage

from econml.dml import SparseLinearDMLCateEstimator

from sklearn.linear_model import LassoCV

est = SparseLinearDMLCateEstimator(model_y=LassoCV(), model_t=LassoCV())

est.fit(Y, T, X, W, inference='debiasedlasso') # X -> high dimensional features

treatment_effects = est.effect(X_test)

lb, ub = est.effect_interval(X_test, alpha=0.05) # Confidence intervals via debiased lasso- Nonparametric last stage

from econml.dml import ForestDMLCateEstimator

from sklearn.ensemble import GradientBoostingRegressor

est = ForestDMLCateEstimator(model_y=GradientBoostingRegressor(), model_t=GradientBoostingRegressor())

est.fit(Y, T, X, W, inference='blb')

treatment_effects = est.effect(X_test)

# Confidence intervals via Bootstrap-of-Little-Bags for forests

lb, ub = est.effect_interval(X_test, alpha=0.05)Orthogonal Random Forests (click to expand)

from econml.ortho_forest import ContinuousTreatmentOrthoForest

from econml.sklearn_extensions.linear_model import WeightedLasso, WeightedLassoCV

# Use defaults

est = ContinuousTreatmentOrthoForest()

# Or specify hyperparameters

est = ContinuousTreatmentOrthoForest(n_trees=500, min_leaf_size=10,

max_depth=10, subsample_ratio=0.7,

lambda_reg=0.01,

model_T=WeightedLasso(alpha=0.01), model_Y=WeightedLasso(alpha=0.01),

model_T_final=WeightedLassoCV(cv=3), model_Y_final=WeightedLassoCV(cv=3))

est.fit(Y, T, X, W, inference='blb')

treatment_effects = est.effect(X_test)

# Confidence intervals via Bootstrap-of-Little-Bags for forests

lb, ub = est.effect_interval(X_test, alpha=0.05)Meta-Learners (click to expand)

- XLearner

from econml.metalearners import XLearner

from sklearn.ensemble import GradientBoostingClassifier, GradientBoostingRegressor

est = XLearner(models=GradientBoostingRegressor(),

propensity_model=GradientBoostingClassifier(),

cate_models=GradientBoostingRegressor())

est.fit(Y, T, np.hstack([X, W]))

treatment_effects = est.effect(np.hstack([X_test, W_test]))

# Fit with bootstrap confidence interval construction enabled

est.fit(Y, T, np.hstack([X, W]), inference='bootstrap')

treatment_effects = est.effect(np.hstack([X_test, W_test]))

lb, ub = est.effect_interval(np.hstack([X_test, W_test]), alpha=0.05) # Bootstrap CIs- SLearner

from econml.metalearners import SLearner

from sklearn.ensemble import GradientBoostingRegressor

est = SLearner(overall_model=GradientBoostingRegressor())

est.fit(Y, T, np.hstack([X, W]))

treatment_effects = est.effect(np.hstack([X_test, W_test]))- TLearner

from econml.metalearners import TLearner

from sklearn.ensemble import GradientBoostingRegressor

est = TLearner(models=GradientBoostingRegressor())

est.fit(Y, T, np.hstack([X, W]))

treatment_effects = est.effect(np.hstack([X_test, W_test]))Doubly Robust Learners (click to expand)

- Linear final stage

from econml.drlearner import LinearDRLearner

from sklearn.ensemble import GradientBoostingRegressor, GradientBoostingClassifier

est = LinearDRLearner(model_propensity=GradientBoostingClassifier(),

model_regression=GradientBoostingRegressor())

est.fit(Y, T, X, W, inference='statsmodels')

treatment_effects = est.effect(X_test)

lb, ub = est.effect_interval(X_test, alpha=0.05)- Sparse linear final stage

from econml.drlearner import SparseLinearDRLearner

from sklearn.ensemble import GradientBoostingRegressor, GradientBoostingClassifier

est = SparseLinearDRLearner(model_propensity=GradientBoostingClassifier(),

model_regression=GradientBoostingRegressor())

est.fit(Y, T, X, W, inference='debiasedlasso')

treatment_effects = est.effect(X_test)

lb, ub = est.effect_interval(X_test, alpha=0.05)- Nonparametric final stage

from econml.drlearner import ForestDRLearner

from sklearn.ensemble import GradientBoostingRegressor, GradientBoostingClassifier

est = ForestDRLearner(model_propensity=GradientBoostingClassifier(),

model_regression=GradientBoostingRegressor())

est.fit(Y, T, X, W, inference='blb')

treatment_effects = est.effect(X_test)

lb, ub = est.effect_interval(X_test, alpha=0.05)Orthogonal Instrumental Variables (click to expand)

- Intent to Treat Doubly Robust Learner (discrete instrument, discrete treatment)

from econml.ortho_iv import LinearIntentToTreatDRIV

from sklearn.ensemble import GradientBoostingRegressor, GradientBoostingClassifier

from sklearn.linear_model import LinearRegression

est = LinearIntentToTreatDRIV(model_Y_X=GradientBoostingRegressor(),

model_T_XZ=GradientBoostingClassifier(),

flexible_model_effect=GradientBoostingRegressor())

est.fit(Y, T, Z, X, inference='statsmodels') # OLS inference

treatment_effects = est.effect(X_test)

lb, ub = est.effect_interval(X_test, alpha=0.05) # OLS confidence intervalsDeep Instrumental Variables (click to expand)

import keras

from econml.deepiv import DeepIVEstimator

treatment_model = keras.Sequential([keras.layers.Dense(128, activation='relu', input_shape=(2,)),

keras.layers.Dropout(0.17),

keras.layers.Dense(64, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(32, activation='relu'),

keras.layers.Dropout(0.17)])

response_model = keras.Sequential([keras.layers.Dense(128, activation='relu', input_shape=(2,)),

keras.layers.Dropout(0.17),

keras.layers.Dense(64, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(32, activation='relu'),

keras.layers.Dropout(0.17),

keras.layers.Dense(1)])

est = DeepIVEstimator(n_components=10, # Number of gaussians in the mixture density networks)

m=lambda z, x: treatment_model(keras.layers.concatenate([z, x])), # Treatment model

h=lambda t, x: response_model(keras.layers.concatenate([t, x])), # Response model

n_samples=1 # Number of samples used to estimate the response

)

est.fit(Y, T, X, Z) # Z -> instrumental variables

treatment_effects = est.effect(X_test)See the References section for more details.

-

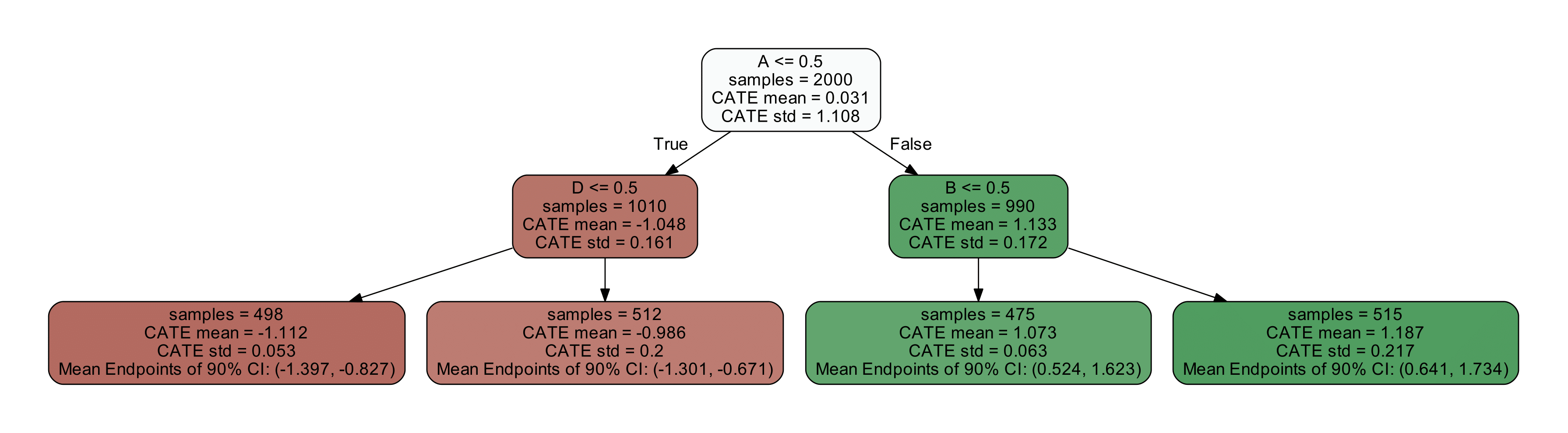

Tree Interpreter of the CATE model

from econml.cate_interpreter import SingleTreeCateInterpreter intrp = SingleTreeCateInterpreter(include_model_uncertainty=True, max_depth=2, min_samples_leaf=10) # We interpret the CATE model's behavior based on the features used for heterogeneity intrp.interpret(est, X) # Plot the tree plt.figure(figsize=(25, 5)) intrp.plot(feature_names=['A', 'B', 'C', 'D'], fontsize=12) plt.show()

-

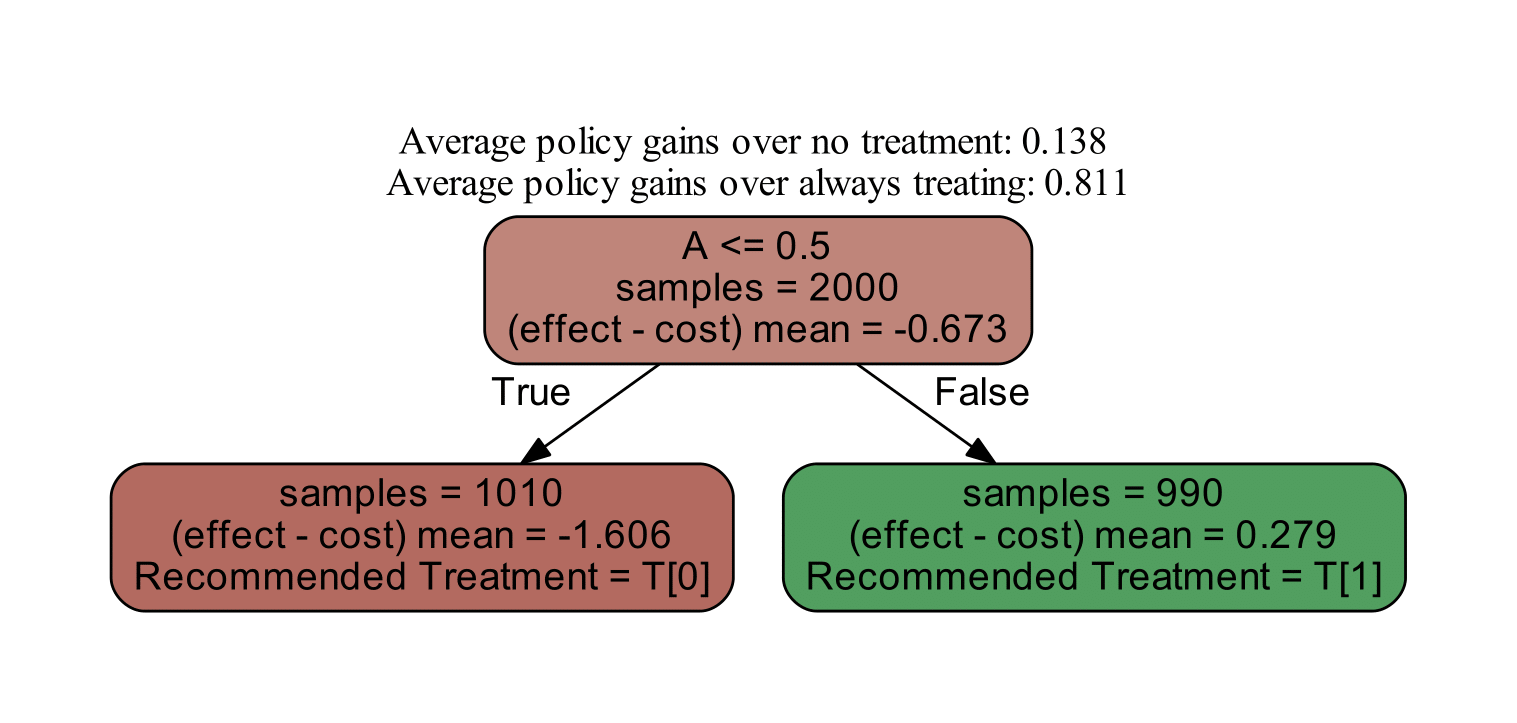

Policy Interpreter of the CATE model

from econml.cate_interpreter import SingleTreePolicyInterpreter # We find a tree-based treatment policy based on the CATE model intrp = SingleTreePolicyInterpreter(risk_level=0.05, max_depth=2, min_samples_leaf=1,min_impurity_decrease=.001) intrp.interpret(est, X, sample_treatment_costs=0.2) # Plot the tree plt.figure(figsize=(25, 5)) intrp.plot(feature_names=['A', 'B', 'C', 'D'], fontsize=12) plt.show()

# Get the effect inference summary, which includes the standard error, z test score, p value, and confidence interval given each sample X[i]

est.effect_inference(X_test).summary_frame(alpha=0.05, value=0, decimals=3)

# Get the population summary for the entire sample X

est.effect_inference(X_test).population_summary(alpha=0.1, value=0, decimals=3, tol=0.001)

# Get the inference summary for the final model

est.summary()To see more complex examples, go to the notebooks section of the repository. For a more detailed description of the treatment effect estimation algorithms, see the EconML documentation.

You can get started by cloning this repository. We use

setuptools for building and distributing our package.

We rely on some recent features of setuptools, so make sure to upgrade to a recent version with

pip install setuptools --upgrade. Then from your local copy of the repository you can run python setup.py develop to get started.

This project uses pytest for testing. To run tests locally after installing the package,

you can use python setup.py pytest.

This project's documentation is generated via Sphinx. Note that we use graphviz's

dot application to produce some of the images in our documentation, so you should make sure that dot is installed and in your path.

To generate a local copy of the documentation from a clone of this repository, just run python setup.py build_sphinx -W -E -a, which will build the documentation and place it under the build/sphinx/html path.

The reStructuredText files that make up the documentation are stored in the docs directory; module documentation is automatically generated by the Sphinx build process.

-

June 2019: Treatment Effects with Instruments paper

-

May 2019: Open Data Science Conference Workshop

-

2017: DeepIV paper

If you use EconML in your research, please cite us as follows:

Microsoft Research. EconML: A Python Package for ML-Based Heterogeneous Treatment Effects Estimation. https://github.com/microsoft/EconML, 2019. Version 0.x.

BibTex:

@misc{econml,

author={Microsoft Research},

title={{EconML}: {A Python Package for ML-Based Heterogeneous Treatment Effects Estimation}},

howpublished={https://github.com/microsoft/EconML},

note={Version 0.x},

year={2019}

}

This project welcomes contributions and suggestions. Most contributions require you to agree to a Contributor License Agreement (CLA) declaring that you have the right to, and actually do, grant us the rights to use your contribution. For details, visit https://cla.microsoft.com.

When you submit a pull request, a CLA-bot will automatically determine whether you need to provide a CLA and decorate the PR appropriately (e.g., label, comment). Simply follow the instructions provided by the bot. You will only need to do this once across all repos using our CLA.

This project has adopted the Microsoft Open Source Code of Conduct. For more information see the Code of Conduct FAQ or contact [email protected] with any additional questions or comments.

V. Syrgkanis, V. Lei, M. Oprescu, M. Hei, K. Battocchi, G. Lewis. Machine Learning Estimation of Heterogeneous Treatment Effects with Instruments. Proceedings of the 33rd Conference on Neural Information Processing Systems (NeurIPS), 2019 (Spotlight Presentation)

D. Foster, V. Syrgkanis. Orthogonal Statistical Learning. Proceedings of the 32nd Annual Conference on Learning Theory (COLT), 2019 (Best Paper Award)

M. Oprescu, V. Syrgkanis and Z. S. Wu. Orthogonal Random Forest for Causal Inference. Proceedings of the 36th International Conference on Machine Learning (ICML), 2019.

S. Künzel, J. Sekhon, J. Bickel and B. Yu. Metalearners for estimating heterogeneous treatment effects using machine learning. Proceedings of the national academy of sciences, 116(10), 4156-4165, 2019.

V. Chernozhukov, D. Nekipelov, V. Semenova, V. Syrgkanis. Plug-in Regularized Estimation of High-Dimensional Parameters in Nonlinear Semiparametric Models. Arxiv preprint arxiv:1806.04823, 2018.

Jason Hartford, Greg Lewis, Kevin Leyton-Brown, and Matt Taddy. Deep IV: A flexible approach for counterfactual prediction. Proceedings of the 34th International Conference on Machine Learning, ICML'17, 2017.

V. Chernozhukov, D. Chetverikov, M. Demirer, E. Duflo, C. Hansen, and a. W. Newey. Double Machine Learning for Treatment and Causal Parameters. ArXiv preprint arXiv:1608.00060, 2016.